Voice AI for BFSI: How Indian Banks Can Automate Millions of Calls

TL;DR , Key Takeaways:

- In FY23-24, 95 Indian banks received over 10 million complaints. RBI is actively pushing for AI-led resolution.

- Six call types dominate BFSI volumes and are all automatable today: EMI reminders, balance queries, loan status, KYC follow-ups, policy renewals, and collections.

- DPDP Rules 2025 and RBI data localization mean borrower audio cannot leave India. On-premise or India-hosted voice AI is the only compliant architecture.

- Indic language voice AI accuracy is the deciding variable. A model producing 25% WER on your callers creates more problems than it solves.

- Shunya Labs Zero STT and Zero TTS cover 55 Indic languages, trained on real audio, on-premise CPU deployment.

A mid-sized private sector bank in India receives between 50,000 and 200,000 customer calls every month. Most of those calls ask about the same things. EMI due dates. Account balances. Loan application status. Policy renewal windows. KYC document submissions.

They follow predictable patterns. The answer is almost always in a database the bank already has.

And yet, thousands of agents spend their shifts answering them. The same questions, hundreds of times a day. In languages that shift depending on which state the caller is in.

Voice AI can change that equation. Not by eliminating human agents, but by handling the calls that genuinely do not need one.

This post covers what those calls are and what it takes to automate them well in Indian BFSI. It also explains why the language and compliance requirements make this harder than most global solutions account for.

10M+

Complaints to Indian banks

FY23-24, across 95 banks (RBI)

$452M

India call centre AI market by 2030

Up from $103.8M in 2024

862M

Agent hours saved globally

Projected by 2026 from voice AI

Why BFSI Has the Highest Call Volume of Any Sector

Banking and insurance generate more customer calls than almost any other industry. The reasons are structural.

Financial products are complex by nature. A home loan, a health insurance policy, a fixed deposit: each carries terms, due dates, and status updates that customers track over months and years.

Unlike a one-time purchase, the relationship is ongoing. Every EMI cycle and every renewal period generates a new wave of inbound calls.

Regulatory obligations make this worse. RBI guidelines require specific disclosures. IRDAI mandates communication touchpoints in insurance workflows. These compliance requirements generate outbound call obligations that banks cannot reduce without regulatory risk. The call volume is, in part, built into the rules.

The staffing situation compounds the pressure. Indian contact centres in BFSI report 30 to 45% annual agent turnover. Every departing agent takes product knowledge and language capability with them. The cost of replacing and retraining that capacity, multiplied across thousands of agents, is significant and recurring.

In FY23-24, 95 Indian banks together received more than 10 million customer complaints. The RBI is now encouraging banks to use AI to sort, tag, and resolve them faster. That is not a suggestion. It is a regulatory signal.

The Six Call Types That Voice AI Can Handle Today

Not all BFSI calls are equal. The ones that work best for automation share two properties. They follow a consistent conversation structure. The correct response already exists in a system the bank already runs.

EMI reminders and payment follow-ups

Outbound reminder calls before an EMI due date can reduce defaults and free the collections team from managing problems that a timely reminder would have prevented. These calls are short and predictable. The agent confirms the date, the amount, and the payment method. A voice agent handles this at scale in any Indian language without adding headcount.

Balance and transaction queries

A caller asking for their current balance or last five transactions needs authentication, a database lookup, and a clear spoken response. This is one of the highest-volume query types in Indian retail banking and one of the cleanest automation candidates. The conversation rarely deviates from a predictable path and the data is always available instantly.

Loan application status

Borrowers call to check where their application stands. Approved or pending? More documents needed? When does disbursement happen? These calls are high in volume and low in complexity. The answer sits in the loan origination system. A voice agent retrieves it and can deliver it in the caller’s language.

KYC follow-ups and document collection

Incomplete KYC is one of the most common reasons customer onboarding stalls in Indian banking. Following up on missing documents, confirming what was received, and guiding resubmission all follow a defined process. Teams at several Indian private banks and NBFCs have deployed voice agents for exactly this workflow.

Policy renewals and insurance servicing

Insurance customers need reminders before their policy lapses and answers about coverage during the renewal window. This is high-value outbound communication that insurers currently run through agent-heavy call centres. Voice AI handles it at a fraction of the cost per contact with consistent accuracy on the disclosure language that compliance teams require.

Collections and soft recovery

Early-stage collections is one of the most widely deployed voice AI use cases in Indian BFSI. The goal here is a payment reminder and a commitment. The call structure is defined, the outcome is measurable, and the economics are clear.

Lead qualification costs can drop from Rs 800 to Rs 120 per lead after voice AI deployment. Overall operational cost per account can fall from 20 to 30%.

The Compliance Layer That Most Solutions Miss

Indian BFSI has strict regulatory requirements. They change the architecture of any voice AI deployment.

Teams that treat compliance as an afterthought end up rebuilding their infrastructure. The time to address it is before deployment, not after.

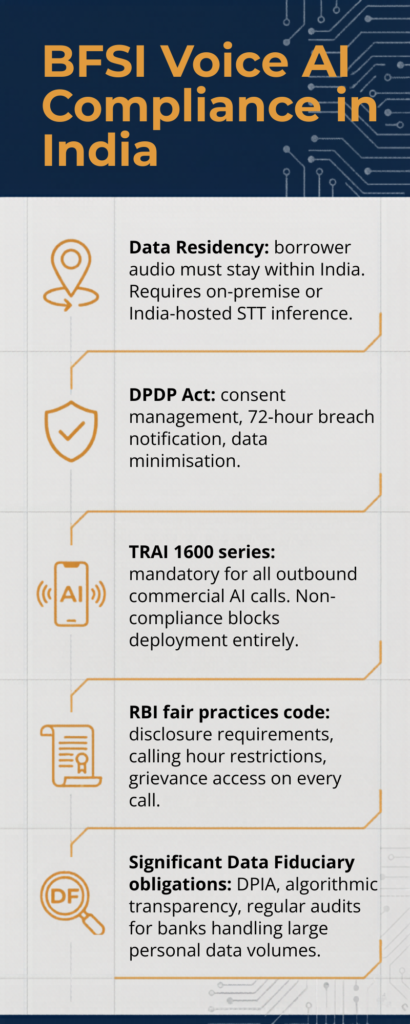

DPDP Act and data localization

India’s Digital Personal Data Protection Rules were notified in November 2025. Under these rules and RBI data localization guidelines, audio containing personal financial data from Indian customers generally cannot be routed to servers outside India. Full substantive compliance is required by May 2027, with the Data Protection Board now operational.

For most global cloud STT providers, this creates a fundamental problem. Their inference infrastructure sits in the US or EU. The audio round-trip adds both latency and compliance exposure. Banks likely classified as Significant Data Fiduciaries face added obligations: Data Protection Impact Assessments, algorithmic transparency, and audit trails. Penalties run up to Rs 250 crore per violation.

TRAI 1600 series directive

From January 2026, TRAI made the 1600 series number mandatory for outbound commercial calls in India. Any voice platform making outbound collections or reminder calls for a bank or NBFC must support DLT-registered 1600 calling. This is a hard requirement. Platforms that do not support it cannot make compliant outbound calls, regardless of everything else they offer.

RBI fair practices code

The RBI fair practices code for lenders sets requirements around how borrower communications are conducted. Calling hour restrictions, mandatory disclosures, accessible escalation paths. A voice agent that cannot reliably follow these rules on every call, in every language, creates regulatory risk that outweighs the operational savings.

BFSI voice AI compliance requirements in India

Data residency: borrower audio must stay within India. Requires on-premise or India-hosted STT inference.

DPDP Act (notified Nov 2025): consent management, 72-hour breach notification, data minimisation. Full enforcement from May 2027.

TRAI 1600 series (effective Jan-Feb 2026): mandatory for all outbound commercial AI calls. Non-compliance blocks deployment entirely.

RBI fair practices code: disclosure requirements, calling hour restrictions, grievance access on every call.

Significant Data Fiduciary obligations: DPIA, algorithmic transparency, regular audits for banks handling large personal data volumes.

Why the STT Layer Determines Whether the Agent Works

The biggest reason BFSI voice AI deployments underperform in India is not the LLM. It is not the workflow logic. It is speech recognition. If the agent cannot accurately understand what the caller said, nothing downstream works correctly.

Indian BFSI callers do not sound like the training data that most global models were built on. They call from mobile phones with variable audio quality. They speak regional languages with real dialectal variation. They switch between Hindi and English in the same sentence. They use financial vocabulary that differs across states and communities.

A global ASR model scoring 5% WER on US English can exceed 25% WER on Marathi, Bhojpuri, or Gujarati telephone audio. At that error rate, one word in four can be wrong.

An agent trying to confirm an EMI amount on audio that broken is not automating the call. It is generating a worse outcome than no call at all.

The only models that work reliably on Indian BFSI audio are built specifically for it. Not adapted from English. Not fine-tuned on a small Indic dataset.

Built from the ground up on real Indian conditions. Telephony compression, regional accents, code-switched sentences, financial vocabulary, and background noise from where real callers actually are.

A voice agent that misunderstands one word in four is not automating your call centre. It is generating more complaints. The STT layer is not a commodity decision in Indian BFSI. It is the most consequential architectural choice you make.

What Good BFSI Voice AI Infrastructure Looks Like

Four requirements define a deployment that holds up in production. These are not aspirational benchmarks. They are the baseline.

Indic language STT trained on real audio

The model needs to have been trained on real Indian phone call data across your specific languages. Word error rate must be measured on production-representative audio, not a global benchmark.

Shunya Labs Zero STT covers around 200 languages. Each is trained on real audio with the dialectal variation, code-switching patterns, and financial domain vocabulary of actual Indian BFSI calls. Independent benchmark data showing 3.1% WER.

On-device deployment without GPU hardware

For teams under DPDP and RBI data localization requirements, audio cannot leave your infrastructure. The model needs to run on-premise, on standard CPU servers, without requiring GPU hardware. The on-device model runs on CPU-only hardware with no GPU requirement. Full deployment guide at shunyalabs.ai/deployment .

Indic model for the voice response

The voice your agent speaks matters as much as what it hears. A caller in rural Maharashtra will disengage from a voice that sounds robotic in their language. Generic models adapted from English produce output that native Indic language speakers can immediately register as unnatural.

Shunya Lab’s model was built natively for Indic languages. Prosody and rhythm are trained on native speakers across all 55 supported languages.

Real-time latency for live conversations

An outbound collection call is a live conversation. If there is an 800ms pause before every agent response, callers start talking over it, repeat themselves, and eventually hang up. Shunya Lab’s streaming latency is under 100ms time-to-first-transcript on production audio. Combined with a right-sized LLM and Zero TTS, total turn latency stays below 650ms. That is within the range where calls feel natural rather than mechanical.

A Practical Rollout Sequence

Most BFSI voice AI deployments can follow a three-phase approach. It helps reduce risk and builds confidence before moving to higher-stakes use cases.

Phase one is outbound reminder calls for EMIs or policy renewals. Volume is high, the conversation is short, and savings are visible within weeks.

The cost difference is stark. Human agent calls in India can run Rs 25 to 40 per call. Automated voice agent calls can run Rs 2 to 3. A bank sending 50,000 reminder calls a month feels that gap within the first week.

Phase two adds inbound balance and status queries. This requires connecting the STT layer to the core banking system through an API. Response accuracy depends on the STT model handling banking terminology correctly in the caller’s language. Amounts, dates, account numbers, all must transcribe accurately for the downstream logic to work.

Phase three, for teams that have validated the first two, is collections automation. This is the highest-value use case and the most scrutinised. Every call must follow the RBI fair practices code. Escalation paths must work. Grievance access must be real and functional. The compliance architecture needs to be in place before collections goes live.

Contact Shunya Labs now to know more.

References

- Basu, S. (2024). Attrition eases in India’s private sector banks. [online] The Economic Times. Available at: https://economictimes.indiatimes.com/jobs/hr-policies-trends/attrition-eases-in-indias-private-sector-banks/articleshow/112691162.cms?from=mdr [Accessed 23 Mar. 2026].

- Grandviewresearch.com. (2026). India Call Center AI Market Size & Outlook, 2030. [online] Available at: https://www.grandviewresearch.com/industry-analysis/call-center-artificial-intelligence-market [Accessed 23 Mar. 2026].

- Malhotra, S. (2025). Sanjay Malhotra: Transforming grievance redress – the AI advantage. [online] Bis.org. Available at: https://www.bis.org/review/r250319j.htm.

- Market, C. (2024). RBI Bulletin: AI revolutionizes Indian banking. [online] @bsindia. Available at: https://www.business-standard.com/markets/capital-market-news/rbi-bulletin-ai-revolutionizes-indian-banking-124103000199_1.html.

- THE INSTITUTE OF COST ACCOUNTANTS OF INDIA (ICMAI) (Statutory Body under an Act of Parliament). (2025). Available at: https://icmai.in/upload/BI/BFSI_CHRONICLE_21st_EDITION_1807_2025.pdf [Accessed 23 Mar. 2026].

Bio: Navvya works at the intersection of product strategy and applied AI research at Shunya Labs. With a background in human behaviour and communication, she writes about the people, markets, and technology behind voice AI, with a particular focus on how speech interfaces are reshaping access across emerging markets.